EACs and Carbon Reduction: Unlocking Compliance with EU CSRD and ESRS

EACs and Carbon Reduction: Unlocking Compliance with EU CSRD and ESRS

Sustainability reporting, nowadays in European countries, has become necessary as a financial reporting for companies. The Corporate Sustainability Reporting Directive (CSRD) instructs that companies disclose environmental and social information with the same thoroughness as financials, highlighting a shift toward full transparency. Harmonizing with this, the European Sustainability Reporting Standards (ESRS) define precisely what should be reported, that is whether it’s greenhouse gas emissions, resource use, or social impact, creating a coherent and comparable sustainability framework across the EU [1].

CSRD, which began taking effect for large companies from 2024, extends reporting obligations far more widely than its predecessor, the Non-Financial Reporting Directive. It requires integrated annual reports, third-party assurance, and links to long-term climate ambitions, such as net-zero by 2050. ESRS, adopted in mid-2023, provides the technical specifications for these reports across a broad range of environmental, social, and governance areas ESG [2][3]. This structured pairing ensures companies’ sustainability stories are both complete and comparable. Below is a table that best illustrates the relationship between CSRD and energy traceability in different areas.

Relationship between CSRD and Energy Traceability in different areas

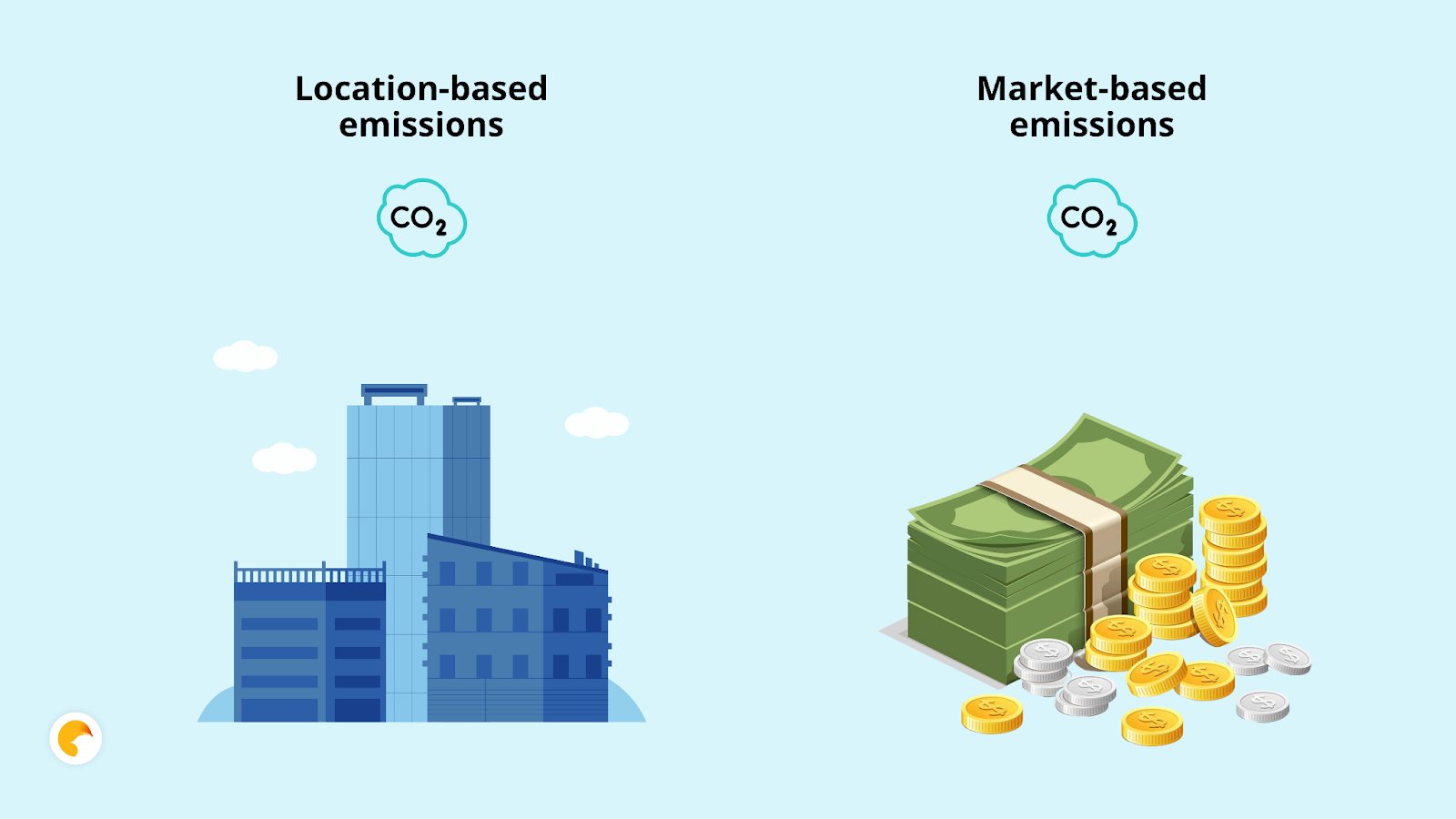

A key focus of ESRS is Scope 2 greenhouse gas emissions, in other words, the indirect emissions resulting from purchased electricity, heating, and cooling. Since Scope 2 can represent a large portion of a company’s carbon footprint and is typically addressable in the near term, ESRS insists on reporting it using two approaches: a location-based method, reflecting grid average emissions, and a market-based method, reflecting the emissions after accounting for renewable energy purchases or contractual instruments [3][4]. This combined reporting captures current realities and corporate efforts alike (see Figure 1)..

Figure 1: Comparison of location-based versus market-based Scope 2 emissions reporting. Location-based shows grid average emissions, while market-based reflects reductions from renewable energy purchases.

At the center of the market-based approach are Energy Attribute Certificates (EACs). In Europe, the primary instrument is the Guarantee of Origin (GO), a digital certification of renewable energy generation. GOs specify key details such as source, date, and capacity, giving them legal weight under EU energy law [5]. Companies can reduce their market-based Scope 2 emissions by retiring GOs corresponding to their energy consumption, symbolically “claiming” the renewable attributes of that energy.

Consider a company using 1,000 MWh of electricity, in this case its emissions on the grid average would be 500 tCO₂. But if it buys renewable certificates (GOs) for 600 MWh, only 400 MWh remain exposed to grid emissions. This lowers its reported emissions to about 200 tCO₂, telling a clear two-part story: the default grid carbon intensity, and the company’s actions to offset it [4][3].

To ensure the integrity of EACs, the GHG Protocol’s Scope 2 Guidance sets strict quality checks. They go as follow:

- Each certificate must show emission data.

- Must only be used once.

- Match the same time period when the energy was used, and come from the same region or electricity grid as the company [6].

These rules prevent double counting and strengthens the credibility of market-based claims.

As companies gear up to file their first ESRS-compliant reports, covering fiscal year 2024 and due in 2025, the narrative should flow naturally: start with the baseline (location-based Scope 2), then showcase action (purchasing and retiring GOs), and conclude with strategic investment toward decarbonization. This progression from reality to responsibility embodies how CSRD and ESRS promote both accountability and ambition [1][2].

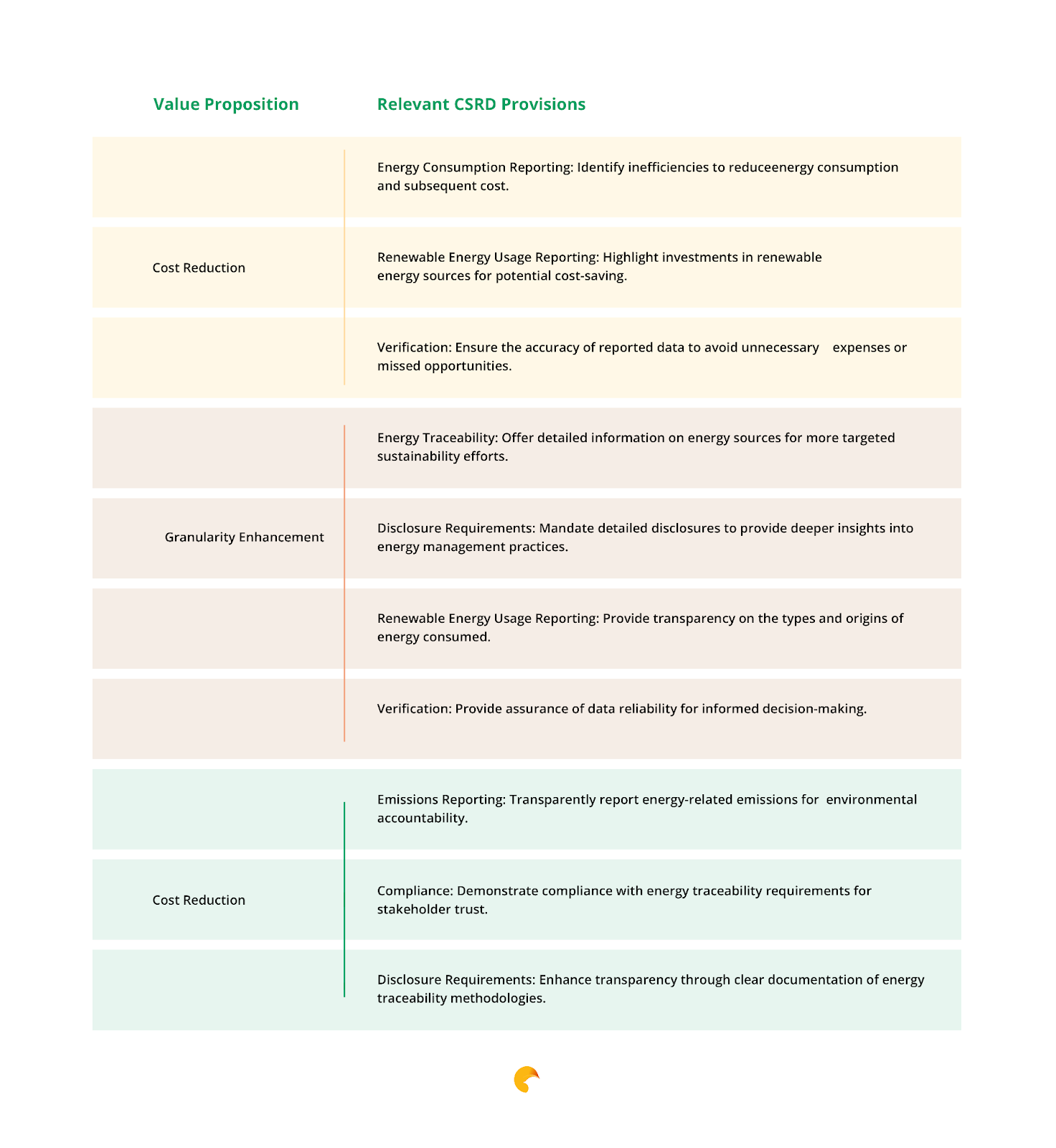

Supporting this transition, Spritju offers a next-generation platform that eases how companies buy, manage, and report Energy Attribute Certificates (EACs). By introducing hourly granularity, Spritju gives businesses unmatched precision in matching energy use with renewable generation, enhancing both transparency and compliance. The platform also delivers up to 20% cost savings in certificate procurement and ensures full auditability through blockchain-backed tracking. In short, Spritju encourages companies to meet today’s reporting requirements while building a smarter, more sustainable energy strategy for the future. The table below illustrates how Spritju's value proposition supports full CSRD compliance by aligning with key reporting criteria outlined in the framework.

Spritju’s Value Proposition in Relation to CSRD

Stay ahead of the latest in sustainability and energy markets with Spritju’s bi-weekly newsletter. We bring you clear updates on CSRD, ESRS, and the smart use of Energy Attribute Certificates to cut emissions and meet EU reporting rules. Get expert tips, market insights, and real examples to help you act with confidence. Together, we can build a cleaner, more transparent energy future, one megawatt at a time.

References

- European Commission – Corporate Sustainability Reporting (CSRD & ESRS Overview)

https://ec.europa.eu/info/business-economy-euro/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en - EFRAG – Sector-Agnostic ESRS & CSRD Development Timeline

https://www.efrag.org/en/sustainability-reporting/esrs-workstreams/sector-agnostic-standards-set-1-esrs - European Commission – CSRD Implementation Timeline, Application Scope, and Reporting Dates

https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en - GHG Protocol – Scope 2 Guidance (Dual Reporting Methods)

https://ghgprotocol.org/scope-2-guidance - Association of Issuing Bodies (AIB) – Guarantees of Origin under EU Renewable Energy Directive

https://www.aib-net.org/certification/certificates-supported/renewable-energy-guarantees-origin - GHG Protocol – Scope 2 Guidance: Quality Criteria for Contractual Instruments

https://ghgprotocol.org/sites/default/files/Scope%202%20Guidance.pdf - European Commission – Q&A on Adoption of ESRS https://ec.europa.eu/commission/presscorner/detail/en/qanda_23_4043

About the Author